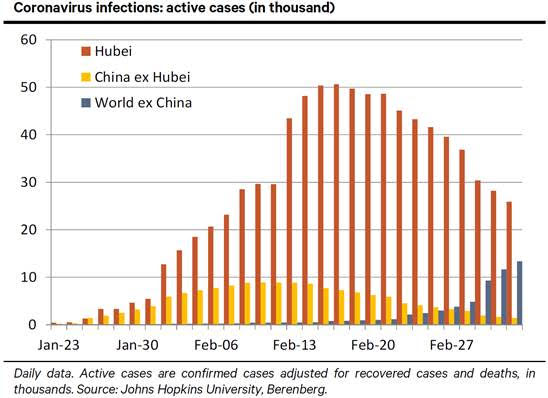

Mixed news: After initially missing the outbreak of COVID-19 in the Hubei region (wave one), China resorted to drastic measures in February. It has reportedly managed to arrest the surge in cases in Hubei and other regions to which the virus had spread (wave two). For now, the first two waves continue to recede. However, the number of active cases outside China is rising steeply in a potentially more dangerous wave three (see chart). Beyond the usual questions about the reliability of Chinese data, we also have to watch the risk that the case numbers in China may go up again when travel restrictions are relaxed and trade with the rest of the world returns to less depressed levels.

Europe is not China: It was on alert early on. Europe contains no Hubei-style region in which the virus could initially spread unhindered. Once China noticed the problem, it took harsh countermeasures that gave other countries valuable time to prepare. The health systems of advanced economies are also much better equipped to cope. In addition, compared with China, citizens in advanced democracies have more trust in their governments. Negative confidence effects in these democracies should, therefore, be somewhat less severe than in China (and Iran). However, a rapid spread in other less advanced regions could add significantly to global risks.

A more measured response: Western democracies are not inclined to impose measures that are as draconian as those in China. That reduces the immediate disruption but could allow the virus to spread further for longer. Western states might, therefore, have to impose prolonged restrictions on day-to-day life and economic activity at a later stage.

Base case: As the – somewhat arbitrary – working assumption for our economic baseline scenario, we expect the situation in Europe, Japan and the US to worsen through April before it starts to improve slightly at some point in May. This implies a near-term recession in Germany, Italy and Japan, a significant risk of a modest recession in the Eurozone as a whole and the UK and below-trend growth in the US in H1 2020. We look for a recovery in H2.

Short-term balance of risks: Amid an evolving medical emergency, the risks to our economic and financial forecasts are much more pronounced than usual. Despite some encouraging signals from China, the near-term risks are heavily tilted to the downside.

Mixed medium-term outlook: Beyond the immediate challenge, two opposing factors will shape the eventual post-coronavirus rebound. As China grapples with serious structural issues – such as an excessive debt load, overly interventionist policies and the natural end of its phase of rapid catch-up growth – it will not support global trade and aggregate demand as much as it did before. At the same time, however, the delayed impact of the fiscal and monetary responses to the epidemic may fully unfold only if and when the virus may already have begun to fade later this year. We thus cannot rule out a stint of above-trend growth in H2 2020. For now, however, we have to focus much more on the disruptions ahead than on the potential shape of the eventual post-coronavirus rebound.

About the Author

Robert - Robert is a private trader with over 15 years experience trading the financial markets.

{kind=link}