Investing in Diamonds?

Before we explore what dictates the price of Diamonds around the world, let’s look at the Geology behind Diamonds. Diamond crystals form deep in the earth’s mantle when carbon is exposed to extreme heat and pressure.

‘Kimberlite’ rocks convey the rocks and crystals from the mantle to the service. The Diamonds and the magma are blasted upwards by eruptions.

Although Kimberlites are associated with diamonds, very few formations have viable reserves. Of 7,000 Kimberlites discovered over the past 140 years only 60 were economic to mine and 7 had substantial deposits.

A report conducted by Petra Diamond Ltd states the chance of finding an economic kimberlite is 1%.

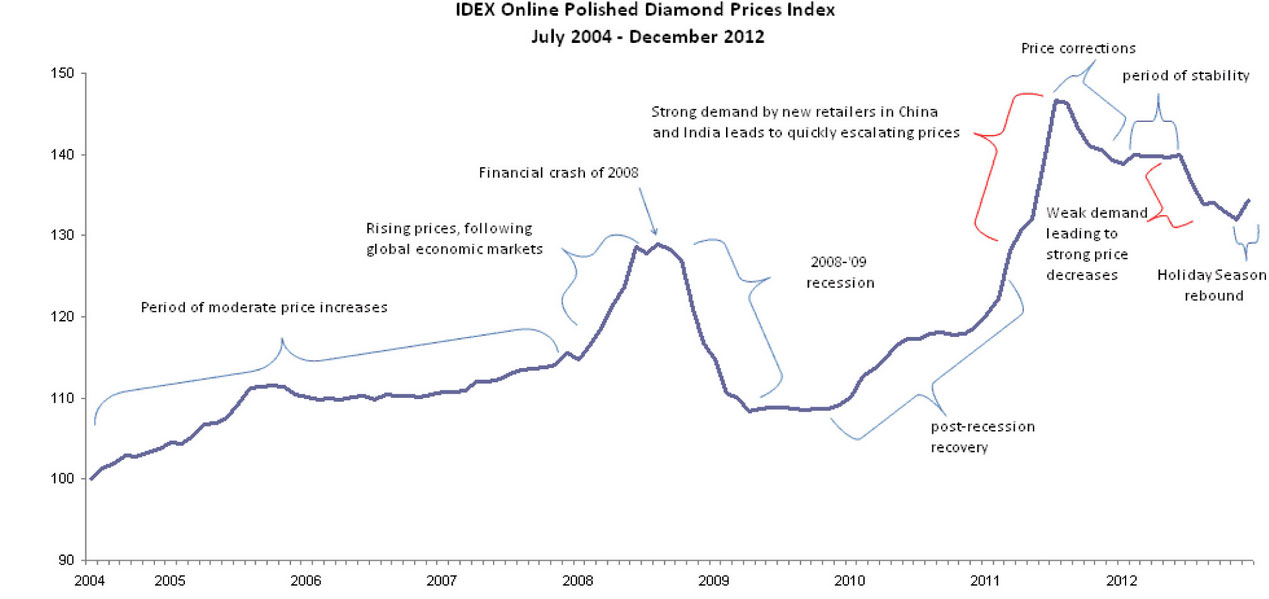

The Economic bit:

To explore the Economics of Diamonds let’s start with some facts:

The USA is currently the largest Diamond consumer, 80% of US couples celebrate their engagement with a diamond engagement ring which is the highest percentage in the world.

The worlds richest deposits of Diamonds are found in Africa, followed by Russia and then Canada.

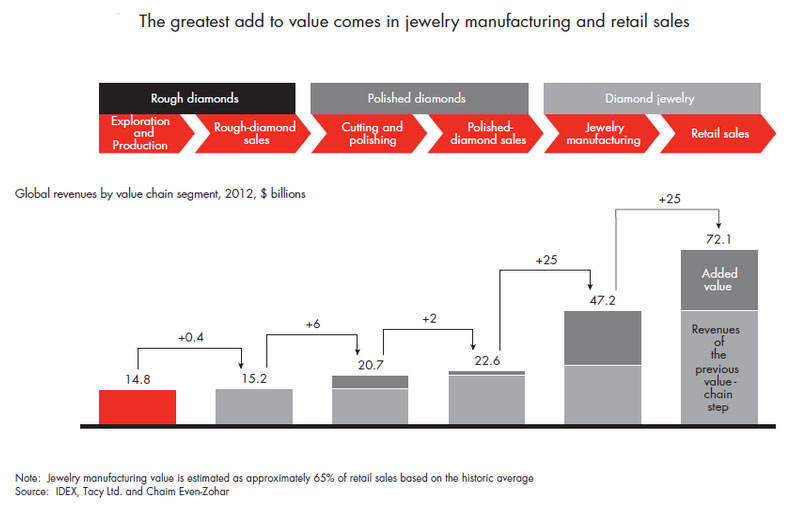

There are many stages of labour in getting a diamond out of the dirt into jewellers windows.

As the Diamonds pass through the 3 stages the price per carat is constantly increasing. Multiplying eightfold or more by the time it is sold at retail. The highest profit margins are enjoyed by the mining company and the end stage retailers.

Diamond price drivers:

Prices are highly correlated to disposable income (the amount of cash you have after buying necessities and paying bills)

Prices are also correlated to inflation rates, the higher inflation the higher diamond prices go.

Supply and demand are the main influential factors –

Supply = the amount of diamonds pulled out of the ground and available for sale.

Demand = the amount of consumers willing to buy.

Studies show in the next 10 years supply is expected to be in line with around a 2% annual increase whilst demand has an anticipated growth rate of 5% – there are reasons for this which we will explain!

First let’s look to supply

As already stated – Economically viable Kimberlites are extremely hard to come by, its accepted within the Diamond industry that the worlds richest deposits have already been discovered. The last major mine was discovered in Zimbabwe 1997.

Supply is expected to grow until 2018, between 2018-2023 experts anticipate that global supply will have peaked and then fall around 1.9% annually due to existing mines being depleted around that time.

What some people may not realise is only 20% of produced rough diamond volume end up as gem quality polished diamonds. 5 carats must be mined in order to produce 1 carat of polished gem diamond. Nearly half of the 5 carat (2.3 carats) are separated out as industrial diamonds (not gem quality) and 1.7 carat is lost in the cutting and polishing process.

Industrial diamond production is declining as technology advances have allowed smaller stones to be cut and polished for jewellery, where as previously they would have been disposed into the “industrial diamond” category which is far less valuable in terms of pricing.

Now lets focus on Demand

We have already stated that personal disposable income is a key in establishing Diamond prices, if everyone in the world didn’t have disposable income then they wouldn’t be able to buy things aside from food, housing etc.

The more people with disposable income the more probability of more Diamond jewellery being purchased.

As a rule – the diamond jewellery market closely tracks the overall luxury goods market. We know the USA is the single biggest diamond consumer, the US economy is therefore a key factor on pricing diamonds.

However, India and China have become emerging consuming nations of Diamonds, with their economies having a boom period, more and more of the population is joining the “middle-class” which means more personal disposable income.

The current (2014) middle class percentage of China is 19% of the population, both India and China have recently observed a slow down in their Economies however by 2023 China’s middle class percentage is estimated to be around the 44% mark.

India’s middle class is ca.16% and expected to grow to around 46% by 2023.

A gradual increase of couples adopting the Western style of engagement ring practice is being observed in India. For keen economists with interests in Diamond investment do keep tabs on the Indian Rupee vs US Dollar.

Diamonds are traded in US Dollars, should the Rupee continue its decline against the US Dollar it makes Diamonds increasingly expensive for the average Indian, thus impacting on demand from India.

All providing evidence that Diamond prices are likely to be positive for the longer term. The key being around 2018 when supply is expected to peak, providing there are no other major discoveries, Diamond prices have the potential to substantially increase.

There are risks that higher Diamond prices may create an industry for ‘recycled diamonds‘ in which diamonds will be recycled back into the market, this would reduce demand however this is arguably an unlikely scenario.

Diamond investment (the direct purchase of the stone to be held as an investment) may disrupt the supply / demand balance and increase prices further although this again is seen as unlikely as diamonds are fairly illiquid investments with the average Joe not being an expert Diamond valuator.

Slow down of the Chinese and Indian economies would likely lead to a decline in diamond demand.

Some Economists argue that supply will cause it’s own demand, the push by growth minded retailers into 2nd 3rd and 4th tier cities and general gravitation into more urban regions will stimulate more diamond jewelry purchases.