Rolling Bets

A rolling bet is a transparent and competitive solution to trading financial products. Bearing a close relationship to the cash market, rolling bets have become very popular in recent years and are a good alternative to trading futures. Rolling bets are available on UK, US and European Equities, Indices, Currencies and some Commodities. Please view the provider’s market information sheets for the full list.

Key Features:

- Rather than expiring at the end of the day, all trades are automatically rolled over to the next trading day.

- Any corresponding orders are automatically rolled over.

- The entry level of the trade remains the same throughout the whole period you keep the bet open.

- A profit/loss is only realised once you decide to close your position.

- Any financing accrued or owed due to holding the product overnight is charged on a daily basis (unlike a quarterly bet where financing is built into the price).

Please note that the spread betting provider may not roll your position if your account were to be in negative equity.

What are daily rolling charges?

Daily rolling charges are fees which are applied to your account on a daily basis for each day you have a daily rolling position open. Because spread trading only requires you to pay a fraction of the cost (i.e. Margin) of the full investment, it means that you are essentially borrowing the balance of funds required. The rollover charge is the interest you are paying on the borrowed money to keep the position open for another day.

Financing Calculation (Except FX)

A position will be subject to financing for each night that it is held open, therefore an applicable product that is held open on a Friday night that is tradable again on Monday, will be subject to financing for 3 days to cover Friday, Saturday and Sunday nights, until the product is tradable once again on the Monday.

Long rolling bets will be charged a financing rate equivalent to LIBOR +2%* (or the equivalent rate depending on the jurisdiction).

Short rolling bets will be credited a financing rate equivalent to LIBOR – 2%* (or the equivalent rate depending on the jurisdiction).

The overnight financing rate is calculated using the following formula:

![]()

Where:

F = Daily Financing

P = Last Closing Price

B = Bet Per

S = stake

I = applicable financing rate

N = day basis (365 for UK, 360 ex UK)

Financing on FX positions is calculated slightly differently and follows the convention of the FX Spot market. Financing to cover a weekend period is normally transacted on a Wednesday evening. You will therefore pay or receive 3 days of financing to hold your position over a Wednesday night to Thursday. Financing over public holidays will also be incorporated into the Spot Next rates and will again be applied according to market convention. Gold and Silver bets pay/receive financing by the same method as the FX financing.

* Please be aware that financing rates and haircuts are subject to change.

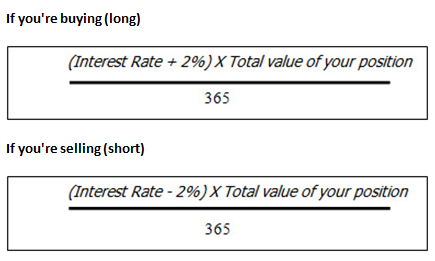

How are daily rolling charges calculated?

If you are short you are paid interest, if you are long you pay interest. Please note the adjustment on a short position can also be negative depending on the prevailing interest rate (generally the 3-month interbank lending rate in the relevant currency. The total adjustment can be calculated using the formula’s below.

What are the currency rollover charges and how are they calculated?

The principal behind FX roll-overs is that you receive the deposit interest of the currency you are long of and pay the borrowing cost of the currency you are short of.

If the interest rate of the currency you are long of is higher than that of the currency you are short of you will receive money.

If the interest rate of the currency you are long of is lower than that of the currency you are short of you will pay.

For Example:

GBP/USD

Interest Rate GBP 0.5% and USD 0.25% Spot Rate 1.5400

Per £1 long:

(0.5 – 0.25 – 2.5) x 15400 / 365 / 100 = -0.94

Per £1 short:

(0.25 – 0.5 – 2.5) x 15400 / 365 / 100 = -1.15

What are the adjustments on rolling futures contracts?

When a futures contract rolls over from one quarter to next, there will be a difference in the closing price of the previous quarter and the opening price of the next quarter. This means that when a client is rolled over into the next quarter, they can artificially make a gain or loss, depending on the level and direction of the price difference between the two quarters. If the opening price of the new quarter is higher than the last then buyers will artificially make a profit from the rollover and sellers will make a loss. If the opening price of the new quarter is lower, then the opposite applies.

In order to reverse out this artificial gain/loss from the rollover, a fair value adjustment will be made to the accounts holding such positions. They will be reflected in their transaction history soon after the rollover.