Signs of an Impending Recession: Commercial Real Estate and Bank Risks

Letter from Palm Valley Capital Management

A rapidly growing bank stores most of its capital in government bills. The market price of its shares soars while the money supply expands rapidly. Inflation rages. The bank’s depositors ask for their money back, but the bank can’t easily satisfy the requests. A bank run ensues, and the bank fails spectacularly. Silicon Valley Bank in 2023? No, this is the 1720 fate of Banque Royale, the engine of John Law’s Mississippi Bubble. Law’s money printing scheme to drive down interest rates was conducted on behalf of the financially desperate French government. At the height of the bubble, Law was the richest and most powerful man in Europe—quite a promotion since he was exiled and condemned to be hanged a quarter century earlier.

The difference between 1720 and now is that in the years following the Mississippi Bubble, an uncontrolled explosion of fiat currency was widely recognized as the culprit for the mess. Today, money creation and haphazard government guarantees are irresponsibly viewed as the solution to our crises. Abe Lincoln said, “Whoever can change public opinion, can change the government, practically just so much.” Thomas Paine we’re not, but we’ll still preach that it’s just common sense to end the country’s longstanding love affair with money printing.

As the fire of the Mississippi and South Sea Bubbles were igniting in the early eighteenth century, another villainous flame was extinguished. Ned Teach, better known as Blackbeard, the world’s most famous pirate, met his violent end off the coast of North Carolina at the hands of British navy soldiers in 1718. He perished by a combination of cutlass slashes and bullets. The Governor of Virginia had Blackbeard’s head hung from a pole along the edge of the James River as a grisly warning to those who might consider piracy. However, public opinion in the colonies regarding pirates was not always negative. From the book Black Flags, Blue Waters: The Epic History of America’s Most Notorious Pirates:

“In the late 1600s, pirates were usually welcomed by the colonies because they brought things of great value that colonists desired and needed; and, better yet, they got them by ransacking Mughal ships sailed by “infidels” in a faraway ocean, or by plundering the hated Spanish in the Caribbean. This meant that, from the colonists’ perspective, piracy was typically seen as a beneficial activity that had little or no downside…The years after the end of the War of the Spanish Succession, however, were an entirely different situation…The days of plundering Mughal ships in the Indian Ocean, and returning to American ports flush with treasure, were long over. Instead, the vast majority of pirates were attacking American vessels off the coast…Rather than supplementing the local economy, pirates were now damaging it. No longer were the pirates the much-beloved fathers, brothers, and friends of colonists who enriched their communities, but rather they were outsiders who, for the most part, brought nothing but strife. Formerly embraced by the colonies, pirates were now seen primarily as a threat.”

Is it farfetched to think that Americans once enriched by the actions of the Federal Reserve and U.S. government in plundering “faraway” people (i.e., future generations) will revolt against these institutions when voters suffer presently? Decisions made in 2020-2021 and prior years contributed to the inflationary upsurge of 2022. Gratifyingly, Fed members finally experienced dealing with a semi-hostile audience.

Today, there are numerous signs of an impending recession and an incipient loss of confidence in the financial system, as the higher interest rates required to quash inflation are exposing deep cracks in the economy. While these fissures can be temporarily mended with emergency stopgap measures, this will only compound the severity of ultimate reset, in our opinion. And don’t forget, almost any disruption to the financial machine has been treated as an emergency requiring a rescue. Like any authentic pirate, regulators would rather go out with a bang than suffer the humiliation of surrendering their wrongheaded policies. Argh, matey, cannons have blown holes in our ship, and we’re sinking into the briny deep. Grab ye a bucket and begin to bail out!

March 19, 2023 Statement by Secretary of the Treasury Janet L. Yellen and Federal Reserve Board Chair Jerome H. Powell: “The capital and liquidity positions of the U.S. banking system are strong, and the U.S. financial system is resilient.”

Some folks have claimed there was no bailout associated with Silicon Valley and Signature Banks because certain executives lost their jobs (after cashing out millions) and stockholders were zeroed. Of course there was a bailout, and we’re not talking about the depositors of these failed lenders. The Fed stepped in immediately with the Bank Term Funding Program to relieve other lenders’ liquidity stress, ensuring the banks would not have to sell assets for, well, what they’re currently worth. Moreover, it didn’t take much pleading from legions of other bank executives before regulators promised, then unpromised, then re-promised to support the depositors of all U.S. banks to stem fears of more runs. Since the FDIC’s reserve fund was a mere 0.7% of the total U.S. deposit base, before recent failures, pledges of support hinge of the power of the printing press.

We have no desire to see unsuspecting depositors lose their shirts due to either banker greed, short-sightedness, or (if you’re feeling charitable) bank runs that cannot be avoided under a fractional reserve system. However, we’re exhausted by “hair of the dog” solutions that perpetuate this cycle of recklessness. The Fed, the Treasury Department, politicians—they’re a bunch of can kickers who act as if any present benefit from their actions outweighs potentially devastating long-term consequences. They’ll hide behind the refrain of supporting jobs that put food on the table tonight, and who could argue with that? They’ll warn, “If we don’t act, we’ll be in another Great Depression.” On the contrary: the situation becomes more combustible with each bailout, as evidenced by the strain already placed on the banking system by 4% interest rates. None of this ever gets better without broad public ire.

Silvergate…Silicon Valley…Signature. If there’s a lesson to be learned, it’s to not start your bank name with “Si”! Encompassing the second and third largest U.S. bank failures ever, many investors are hoping the downfall of these lenders can be pinned on cryptocurrency or venture capital exposure, an abnormally high percentage of uninsured (and therefore uncomfortable) deposits, or unique asset/liability mismatches. The March distress spread to First Republic Bank, another West Coast lender with significant uninsured deposits, then Credit Suisse, a once-venerable institution that had been foundering in recent years. Credit Suisse was taken over by UBS during a hectic weekend in a rush job arranged by the Swiss government.

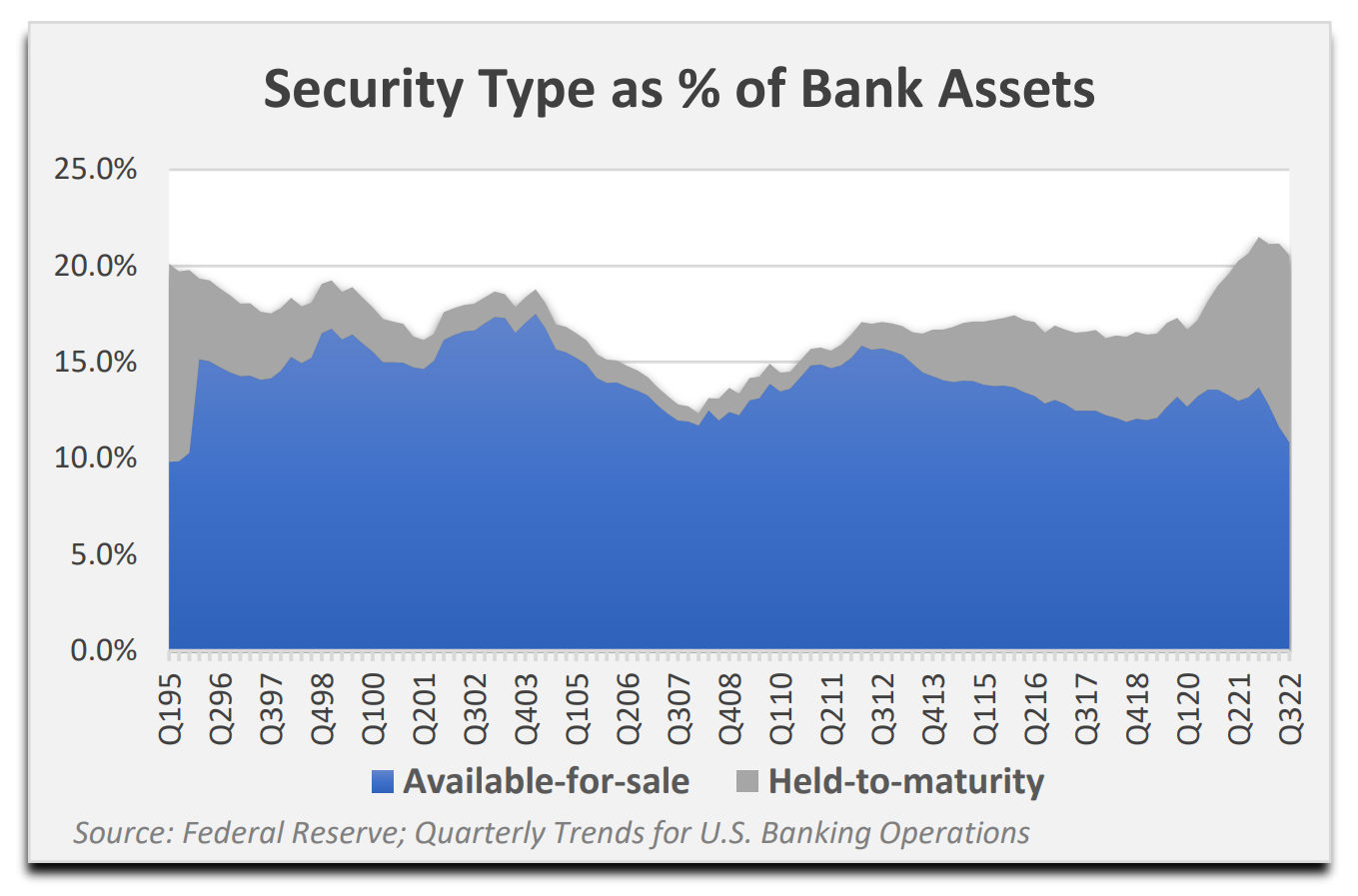

While it was hard to keep up with the pace of developments in the sector, it should be clear that banks are opaque businesses. As one example, over the last decade, the percentage of domestic bank assets represented by held-tomaturity (HTM) securities increased significantly. This phenomenon obscures measures of shareholders’ equity in volatile rate environments, since HTM securities are carried at cost. Although the fair value of these securities can be ascertained by reading financial statements, it’s much harder to know the true value of bank assets with credit risk. Loans, as Level 3 assets, are assigned a fair value based on management’s assumptions about the assumptions that market participants would use in pricing an asset or liability. Shiver me timbers!

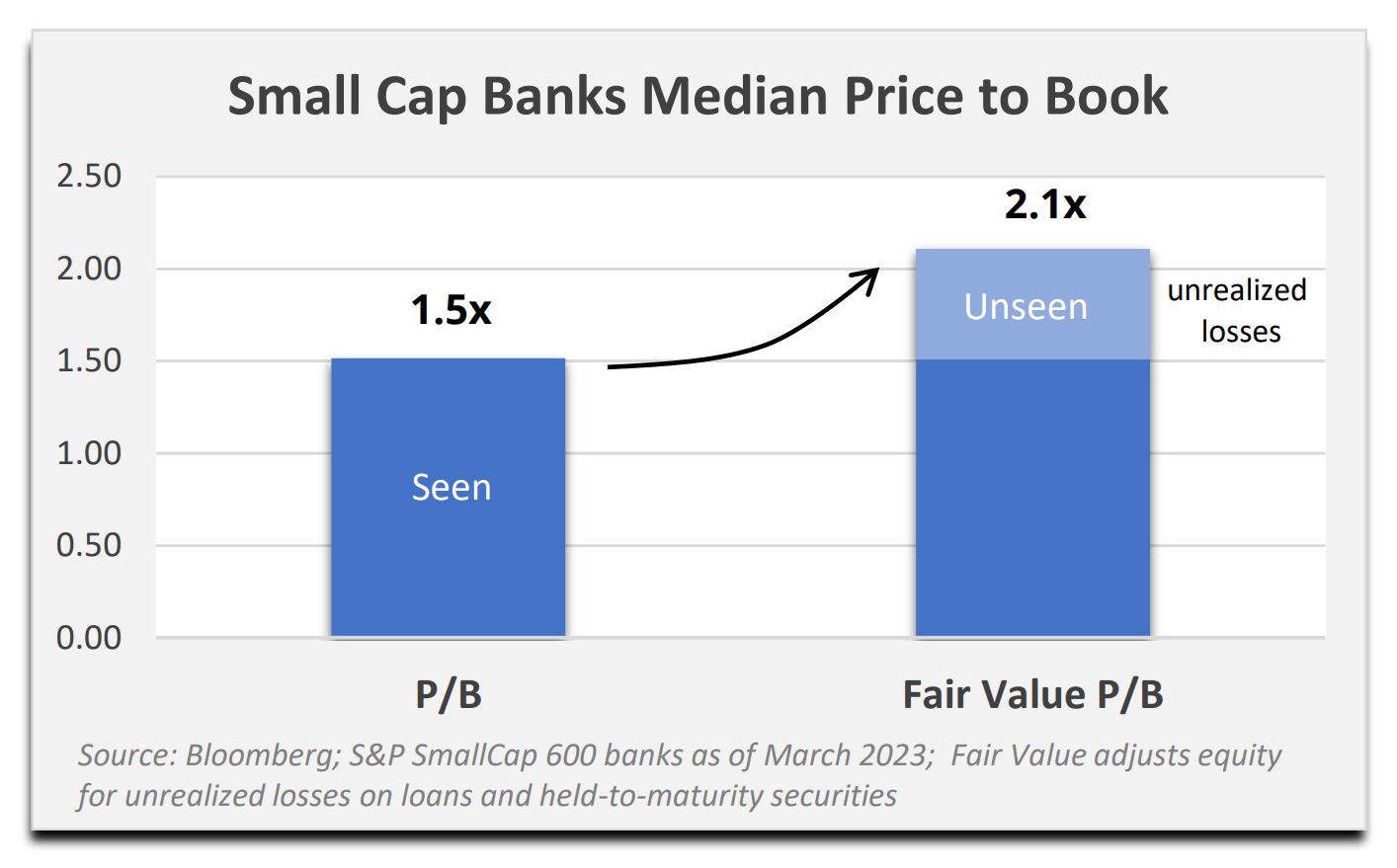

Historically, we have generally only purchased banks trading below book value. We must believe shareholders’ equity is reasonably solid and unlikely to suffer a material impairment in an economic downturn. Given the significant increase in small cap bank exposure to commercial real estate during this market cycle, we believe balance sheet risk has increased considerably. As a result of our criteria, we haven’t owned many small cap banks. Even now, after a threatened banking crisis, the median Price to Book (P/B) multiple for banks in the S&P SmallCap 600 Index is 1.5x. If we adjust book value to account for unrealized losses on held to-maturity securities and loans, the median P/B ratio grows to 2.1x.

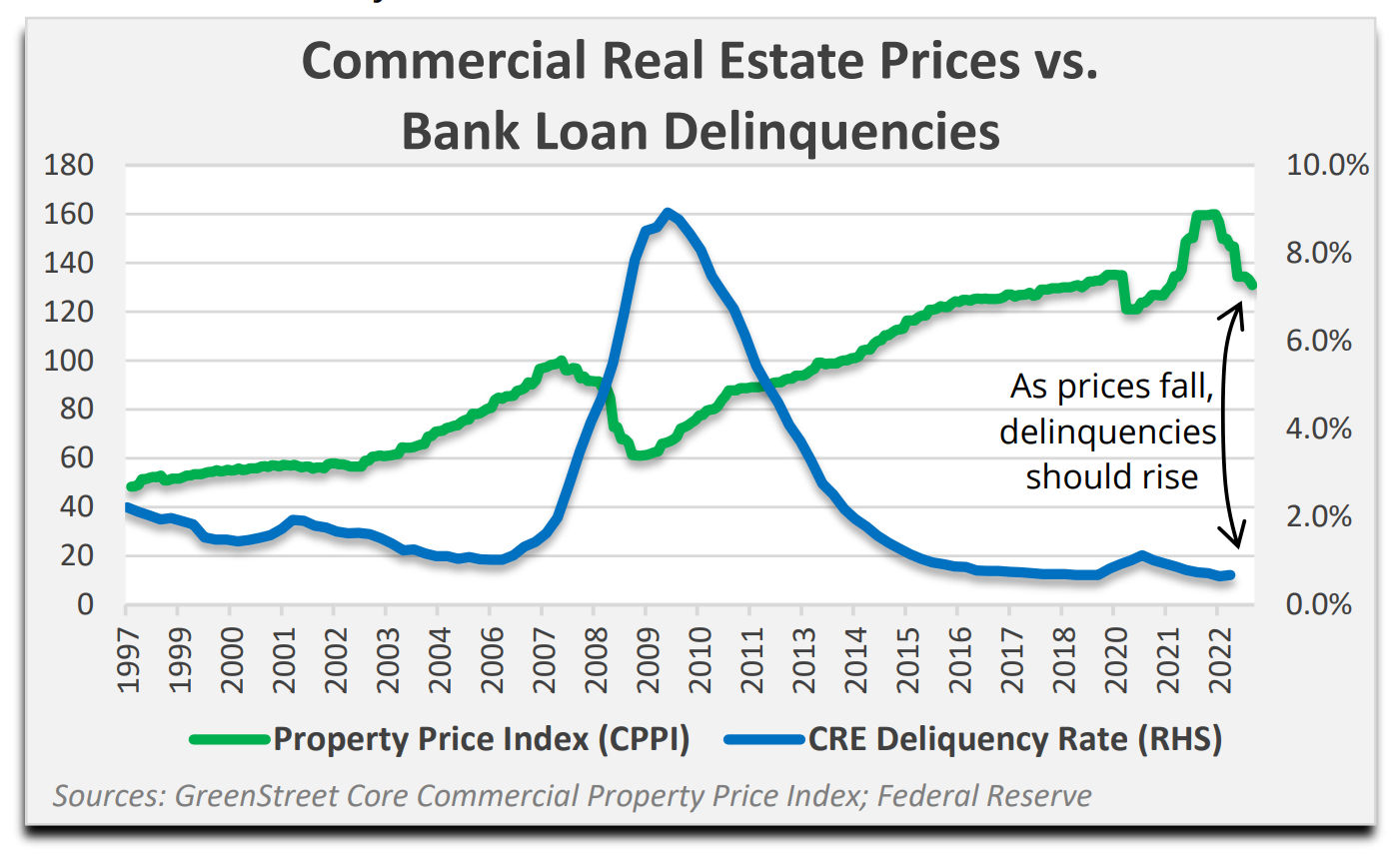

Commercial real estate, including multifamily and construction loans, represents almost 5x the equity of the average small cap bank! The Blackstone REIT (BREIT) drama is another recent example of the friction that can occur when you combine an illiquid asset class (real estate) with investors who want their money back immediately. Delinquencies on commercial property loans, as reported by the Fed, were still at record lows in the fourth quarter of 2022 but have begun to creep higher. Several high-profile investors have defaulted on office properties in major cities, a consequence of pandemic work from home trends that never fully reversed. Over $1.4 trillion of commercial real estate (CRE) debt will mature by the end of 2024 (Mortgage Bankers Association), more than 30% of outstanding loans, prompting at least one real estate CEO to shamelessly request an industry lifeline from regulators. We think the smooth sailing is finished. First Republic Bank and Signature Bank have/had the 9th and 10th largest CRE loan portfolios, respectively (Trepp).

More than half of S&P SmallCap 600 banks reported a decline in net income in 2022, but the median decrease was only 2%. Small cap bank earnings are still up more than twofold, on average, over the past five years. The current 10x P/E for the typical small bank is deceptive, since it is predicated on low-cost deposits that are now seeking higher yields and/or safer homes. U.S. banks began losing deposits at the fastest pace ever beginning in the second quarter of 2022. Several of those low P/E lenders have no shareholder’s equity at all when assets are marked to fair value (Level 2 and Level 3 accounting basis). Whether or not banks work out as an investment from here, based on our experience, banking is an extremely leveraged business model reliant on government backstops.

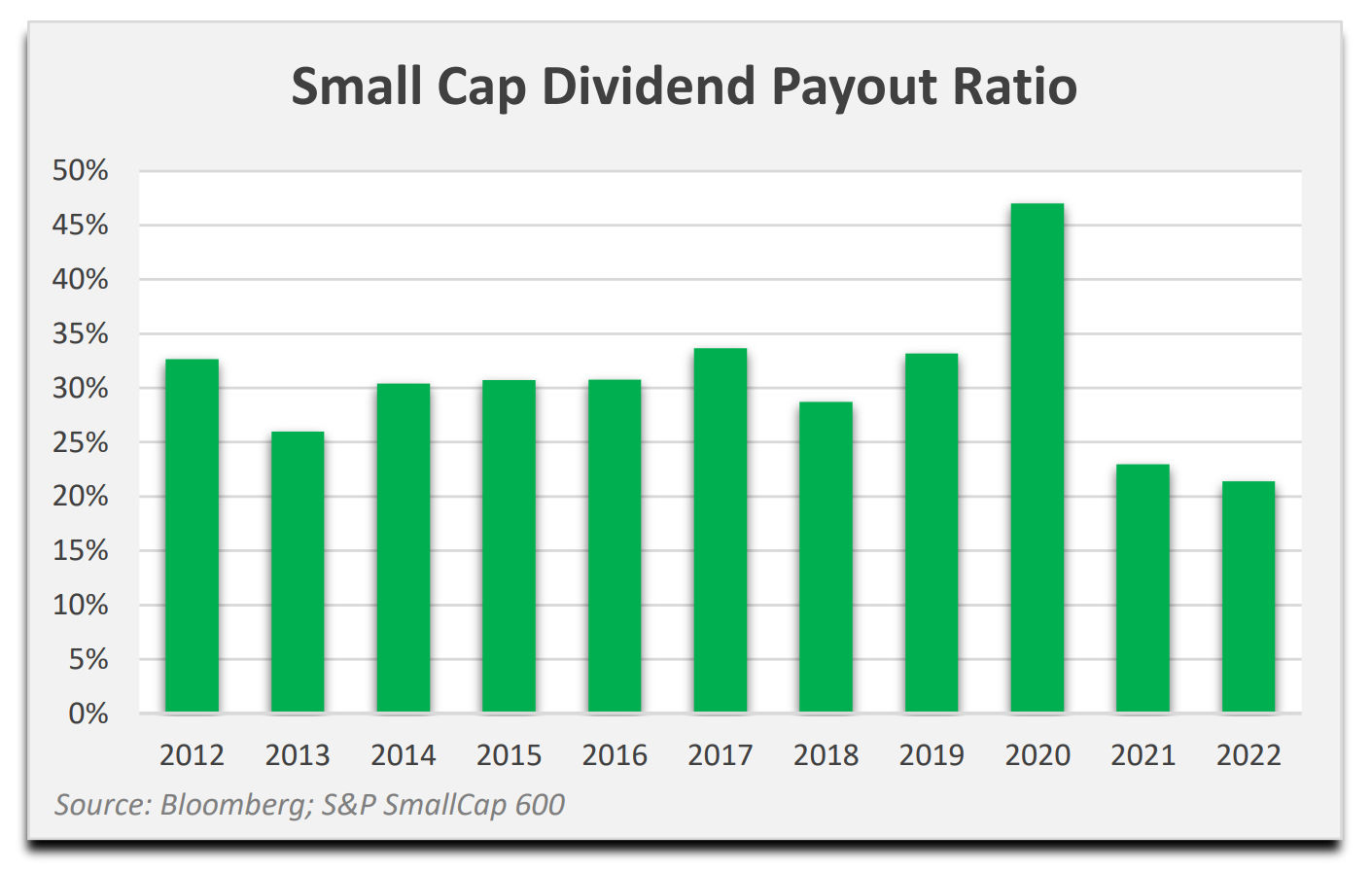

Determining normalized profitability is sometimes more art than science, but we believe it’s still a critical task for absolute return investors. It’s perfectly acceptable to use trailing earnings as a starting point for normalization, since it has the advantage of inflation baked in. Yet, stopping there would often be a mistake. During our diligence, we ask why the past year may not be reflective of typical economic conditions and earnings power for a business. From our perspective, 2021-2022 is an unambiguous outlier of excess profitability driven by record deficit spending. Even management teams do not appear to be buying the sustainability of trailing profits, as average small cap dividend payout ratios are at the lowest levels of the last decade.

The normalization exercise gets trickier when rewinding further. We believe this entire economic cycle has been distorted by low interest rates, debt, and overall financialization. Even so, the further back one goes to search for a so-called normal economy, the more disconnected the business under review might be relative to its present status. Has the company acquired, lost a major customer, developed a new product or service line, etc.? It can help to focus on operating margins over time instead of nominal earnings. We will determine the average full cycle operating margin for a business and apply this to our best estimate of normalized revenue. For many businesses, including some in our Fund, we project normalized sales below what has been achieved for the past twelve months. This may seem noteworthy given the inflation experienced throughout this period and reflects our views on sustainable demand.

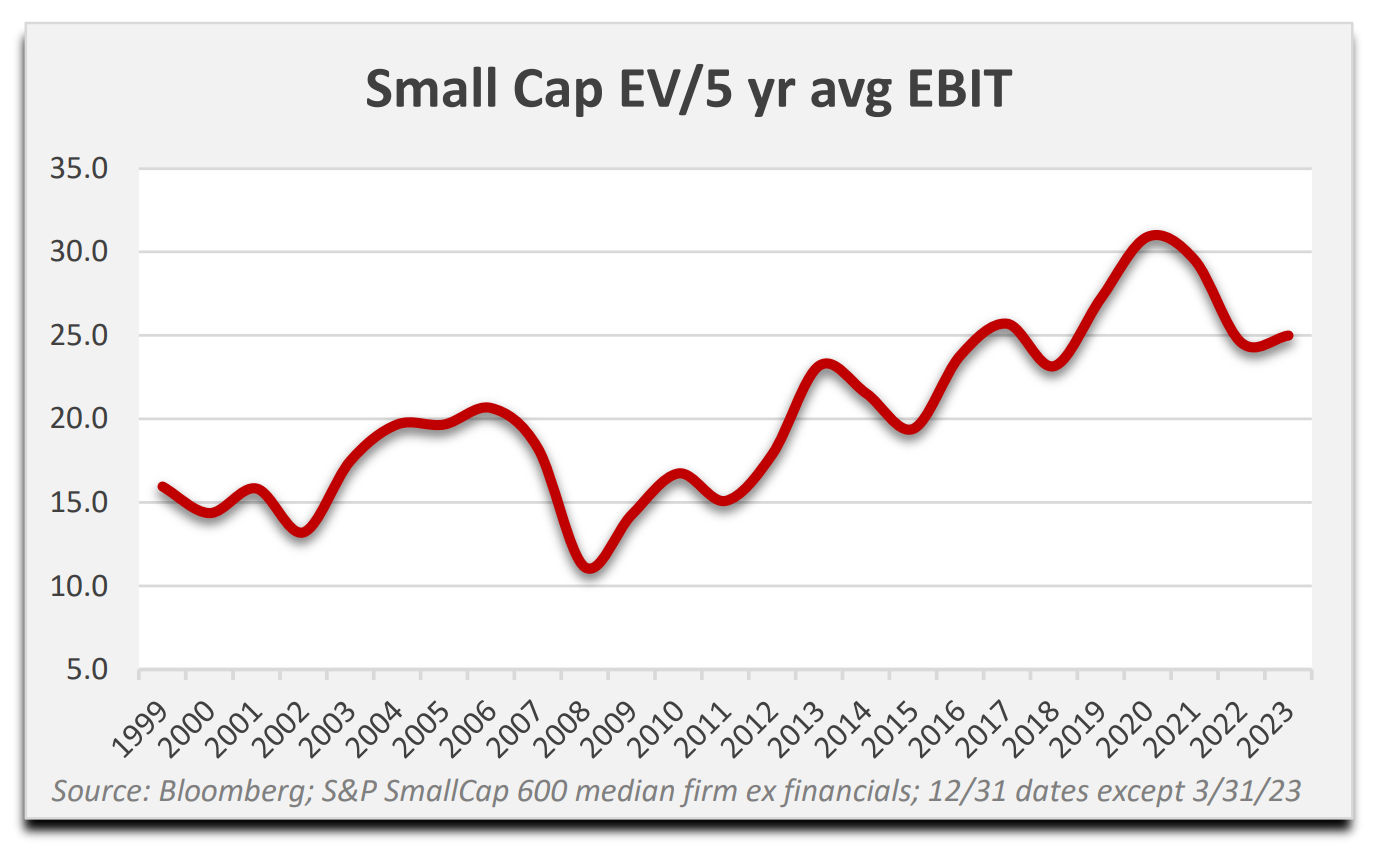

Although we spend a significant amount of time dissecting any company we consider purchasing for the Fund, for the purposes of these letters, we tend to generalize to simplify communication. A crude attempt to normalize operating profits could be to take a five-year average. Honestly, this seems overly generous for many businesses, but it at least includes a temporary dip in earnings in 2020. On those grounds, we submit that higher quality small caps are still far from cheap. The median small cap is trading for 25x its five-year average operating profit (S&P 600). Reported small cap earnings have fallen 7% from their 2022 peak, in contrast to large cap earnings (S&P 500), which may be cresting, but haven’t reversed yet.

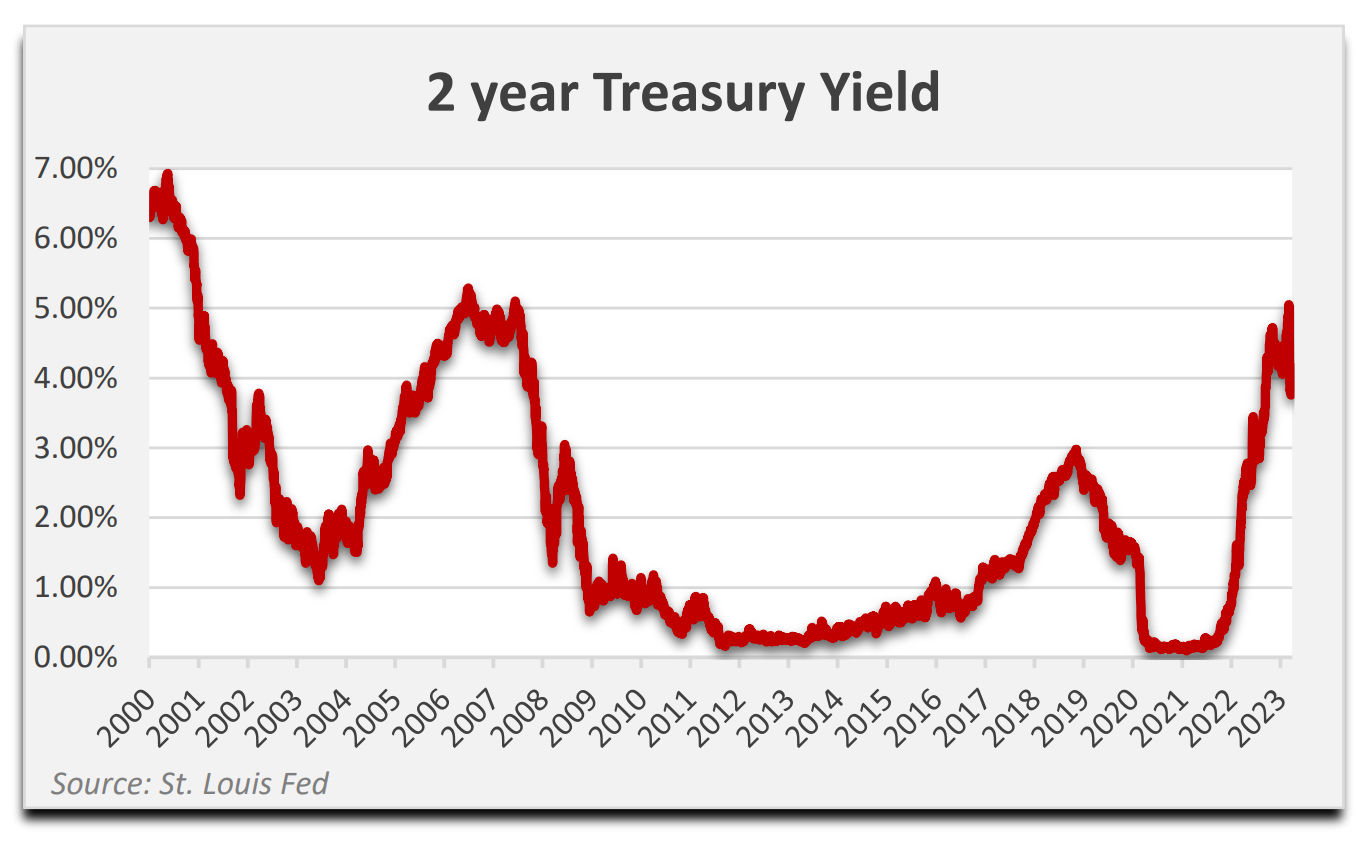

We heard for many years that there was no alternative to owning equities. It’s been harder to make that argument recently with rising short-term risk-free yields, which peaked above 5% in early March before collapsing to below 4% on bank contagion fears (2-year Treasury). Despite telegraphed rate increases from the Fed throughout 2022 and year-to-date, most investors stayed faithful to their equity allocations. Dance with the one that brought you, right? Their core belief is that lower rates are the elixir for all that ails capital markets, and that the alchemists at the Fed will not withhold their magical potion for much longer. Rate cuts could fix bank balance sheets and bring back deposits. ZIRP is manna for equities, bonds, and real estate. Many in Congress are already demanding monetary easing in the name of supporting employment. Concerns about inflation have been displaced by fears of bank runs and economic instability. Meanwhile, the Fed is assuring us it will finish the job on inflation before reversing policy.

At the end of the day, we believe asset prices are the tail that wags the dog of Fed decisions. Indefatigable equities have not yet exhibited the same volatility as interest rates. We see no credible reason why this business cycle won’t conclude with the decline in corporate profits and the low valuations we’ve seen time and again over history. Batten down the hatches, something has got to give.

On the one hand, tighter monetary policy has caused a reduction in speculative activity. Trading on the online broker Robinhood has fallen precipitously since the pandemic. The number of IPOs is down 90% from 2021. Certain meme stocks, like Bed Bath & Beyond, are approaching the dustbin. On the other hand, investors remain emboldened by strong corporate profits, and equity prices are still fanciful versus most historical comparisons. In 2023, despite interest rate volatility and fears of a brewing banking crisis, speculators are entranced by newish playthings like 0DTE options, which accounted for over 40% of total options activity in March (Bank of America). Bitcoin is up over 70% in 2023 after tanking last year. The NASDAQ has gained 17% year-to-date.

During the Golden Age of Piracy, which lasted from 1650 to 1730, convicted buccaneers were hanged in a public square. To maximize suffering for heinous offenders, a short rope was sometimes used so the criminal’s neck wasn’t snapped instantly when the scaffold dropped. They would instead slowly asphyxiate. “Dancing to the four winds,” also known as “dancing the Tyburn jig,” was a colloquialism for the brief period when the condemned pirate remained conscious and their legs would desperately kick. Many investors are praying that bank rescues, a rapid re-expansion of the Fed’s balance sheet, and a rush of inflows back to big tech stocks are embers that can stoke a renewed bull run. Not us. We’re out seeking justice in the town square, hoping we’re watching the final convulsions of the Everything Bubble. The crowd is sparse but growing. For everyone’s sake, we hope the eventual carcass of this market cycle, whose orchestrators have plundered repeatedly from the future, will serve as a lesson that lasts for generations. Dead bubbles do tell tales.

{kind=link}