Has the Long-Awaited Rebound Started in the Bombed Out Fashion UK eCommerce Sector?

Has the long-awaited rebound started in the bombed out fashion eCommerce sector, or is this a dead cat bounce?

ASOS just released a trading statement today with the following as a summary:

Trading Statement – is the 4 months to 31 Dec 2022, of FY 8/2023.

ASOS (ASC) –

ASOS reported a 3% fall in revenue over the four months to the end of December “reflecting challenging trading conditions and prioritisation of structural profitability improvements”. Adj gross margin broadly flat with encouraging progress through the period. ASOS was hurt by weaker demand and delivery disruption in its biggest market Britain and making it one of the laggards in the sector.

Britain is currently suffering a cost-of-living crisis but other retailers with physical shops like Next PLC outperformed ASOS in the period as consumers prioritised festive spending and chose to visit stores rather than worry about delivery issues. ASOS said UK sales were down 8% in the period which it blamed on weak consumer sentiment, earlier cut-off dates for Christmas deliveries due to the delivery problems and a tough comparison against last year when the pandemic favoured online.

Q1 revenue down 4% vs LY. Reckons it can make profit improvements of >£300m, more than offsetting inflationary headwinds & higher returns rate. FY guidance is cash outflow of £(100)m to zero range – doesn’t seem very good, despite the upbeat commentary. Expecting an H1 loss, with significant improvement in H2. Stock write-off was previously c.£90m, now increased to c.£130m, buried in footnote 2. Low gross margin of 42.9%, and only 36.1% after including stock write-off. Says this will improve, it needs to! So the H1 numbers are likely to look awful, but we’re served jam tomorrow for H2 & beyond.

Paul Scotts (Market Analyst) opinion: I’ve heard for years that Asos grew exponentially fast, but was a shambles internally – as people, systems, processes, didn’t change with the growth. Today’s indication of £300m+ cost-savings and profit improvements shows that they’re at last taking decisive action to make this a profitable business (it’s never really made any sustainable free cashflow [just a blip in the pandemic], and has never paid divis). Massive £4bn revenues means that every 1% of extra margin puts c.£40m onto the bottom line. Gross margin has always been far too low at Asos. Reduction in costs could further improve profits. So I can see there’s a decent opportunity here, it could be an interesting trade, but it’s too early to judge whether it will make a good long-term investment or not.

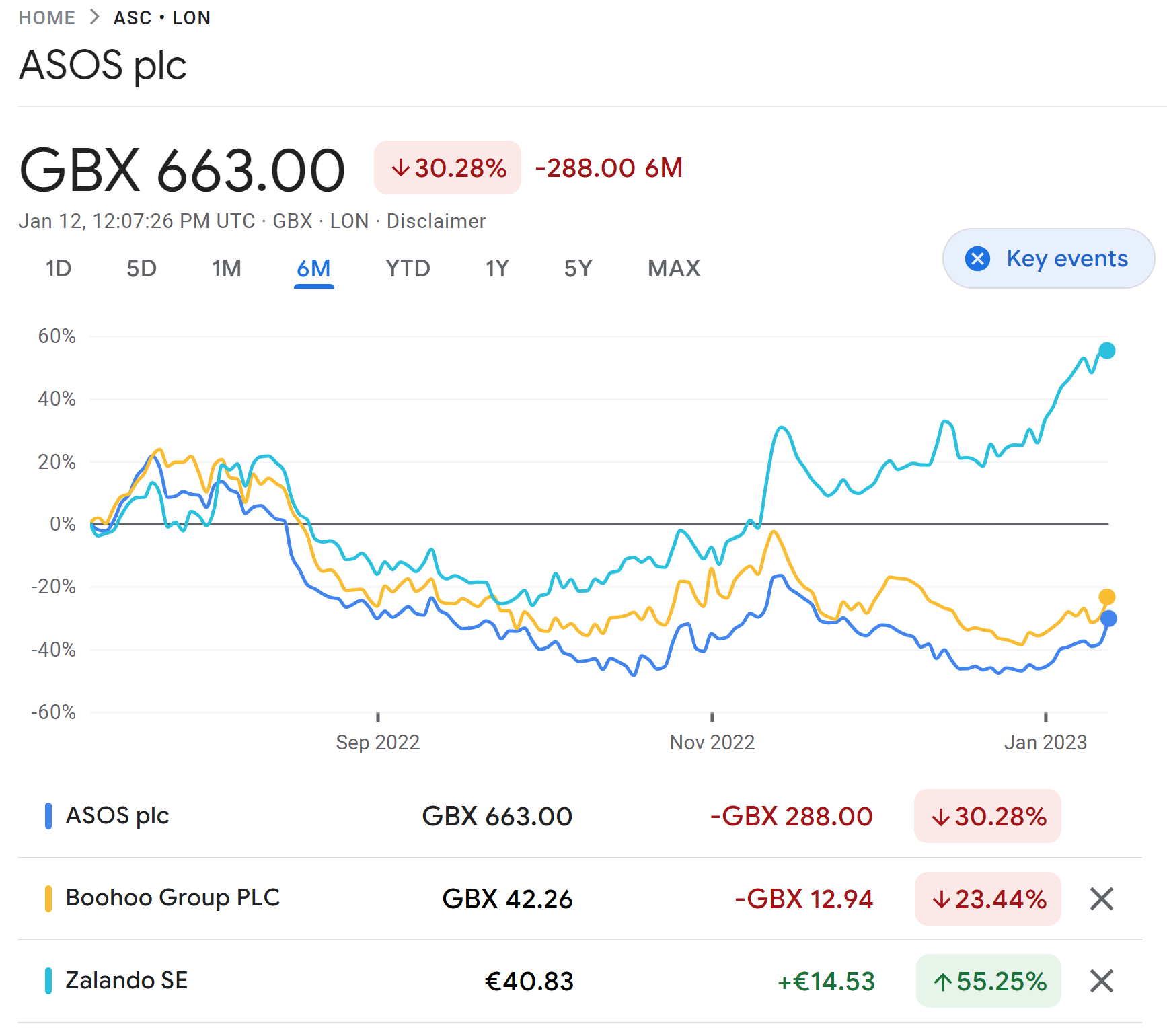

Looking at comparisons of on-line retailers UK versus Europe based, it seems an upward trajectory is occurring. The European retailer Zalando SE (ETR:ZAL) seems to have taken an upward trend earlier than the two UK based retailers ASOS (LON:ASC) and Boohoo (LON:BOO).

{kind=link}