Home Ownership versus Renting a Home

Is it better to own a house by taking a long term mortgage loan or does renting make better sense?

Ok, here’s one I’ve struggled to change any lay person’s mind about, that makes me very scared for the future of society—

Somehow, the majority Americans still seem to believe home ownership is always more financially sound than renting (if you can afford a down payment).

When I propose that is often not the case, they explain— usually in a condescending manner— that…

- Mortgage payments (on a 30 year loan) are less than monthly rent for a similar property. In my head, every time: “It… doesn’t work like that…”

- Paying rent is throwing money away, unlike a mortgage. “Stay cool Zach… stay cool…”

- Property generally appreciates, and you can’t realize those gains if you are renting. “Zach— don’t bother! Zach! Leave it… Let them be.”

- Home ownership is the American dream!!! “Sigh…”

I am probably 25% into this answer and haven’t decided how far I will go in making a case for renting… It usually doesn’t go well, even with relatively financially savvy friends.

But understand this—

On the side of people who benefit from perpetuating these myths— no, generalities— you have…

- Real estate agents

- Mortgage lenders

- Insurance companies

- Mortgage-Backed Securities (MBS) investors

- Every company that supplies home improvement products & services, that benefits from such a fragmented buying pool

- Etc, etc

Now, who is incentivized to persuade people to rent?

- Renter’s insurance providers

- A very fragmented property management industry

- ???

So, several industries with a combined market cap in the trillions on one side…

Who is going to out-spend, and out-communicate the message that benefits themselves, here?

I hope I don’t have to answer that for you.

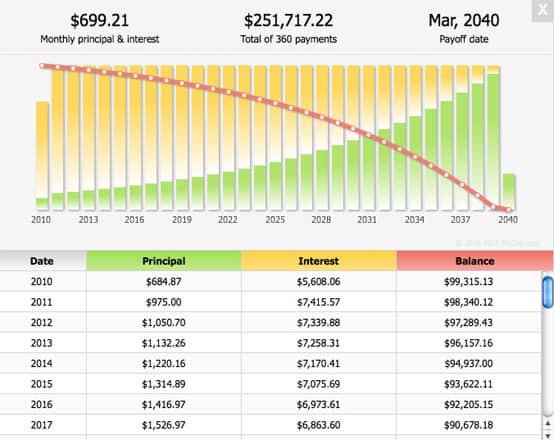

Let’s begin with an amortization table.

Here we have a 30-year, $100,000 mortgage, 7.5% interest, taken out in 2010.

Notice that in 2017, $90,678 still remaining in principle after making ~ $65,000 in payments.

So, in 2017, something like 93% of your payments have been interest. That changes over time… over 30 years.

Who the hell owns a house for 30 years?

I’m not googling it, but I’m guessing the average person sells their house after 5 years, paying a 6 percent commission to the agents (if you sell your house when you need to).

Then there’s all that insurance you paid, the repairs & maintenance, closing costs, etc etc.

Moving on—

Often the same ‘wise old people’ who insist you buy a house if you can afford it, no matter what, will also give further unsolicited advice about “investing in the stock market.”

Oh boy…

“You have to be diversified…” they say… “you can’t put all your eggs in one basket. What if the company goes bankrupt?”

“But Mr.— didn’t you just tell me I should buy a $330k house with 10% down? Where 90% is the banks money?”

“Yea, Jimmy, I said that. What? Do you need to get your ears cleaned? Yeesh.”

Ok so now Jimmy puts the $10k he has left into a perfectly, wonderfully diversified stock portfolio.

And Jimmy’s total “diversified portfolio” looks like this…

- $9k S&P 500 index fund

- $1k global bond fund (I’m assuming Mr. gave you a little bit of sound advice here— bear with me— well, as long as Mr. didn’t send Jimmy to Edward Jones where he paid a 4% fee upfront)

- $30k real estate equity (1 property)

- $297k mortgage debt at 5% interest

- $30k student loan debt

…5 years later…

Mr: “So Jimmy, how about that student loan crisis? Millennials blah blah lazy blah blah sensitive blah blah liberals blah blah my generation blah blah”

Jimmy: “Yea… about that… my house is now worth 20% less— $264k— I still owe $280k on it. I lost my job. I haven’t been able to make payments on my student loan…”

Mr: “Jimmy, you’re living the American dream. Quit complaining and work a little harder, would ya? Damn millennials…”

I need a drink… to be continued… maybe…