Brexit: Trading Opportunities

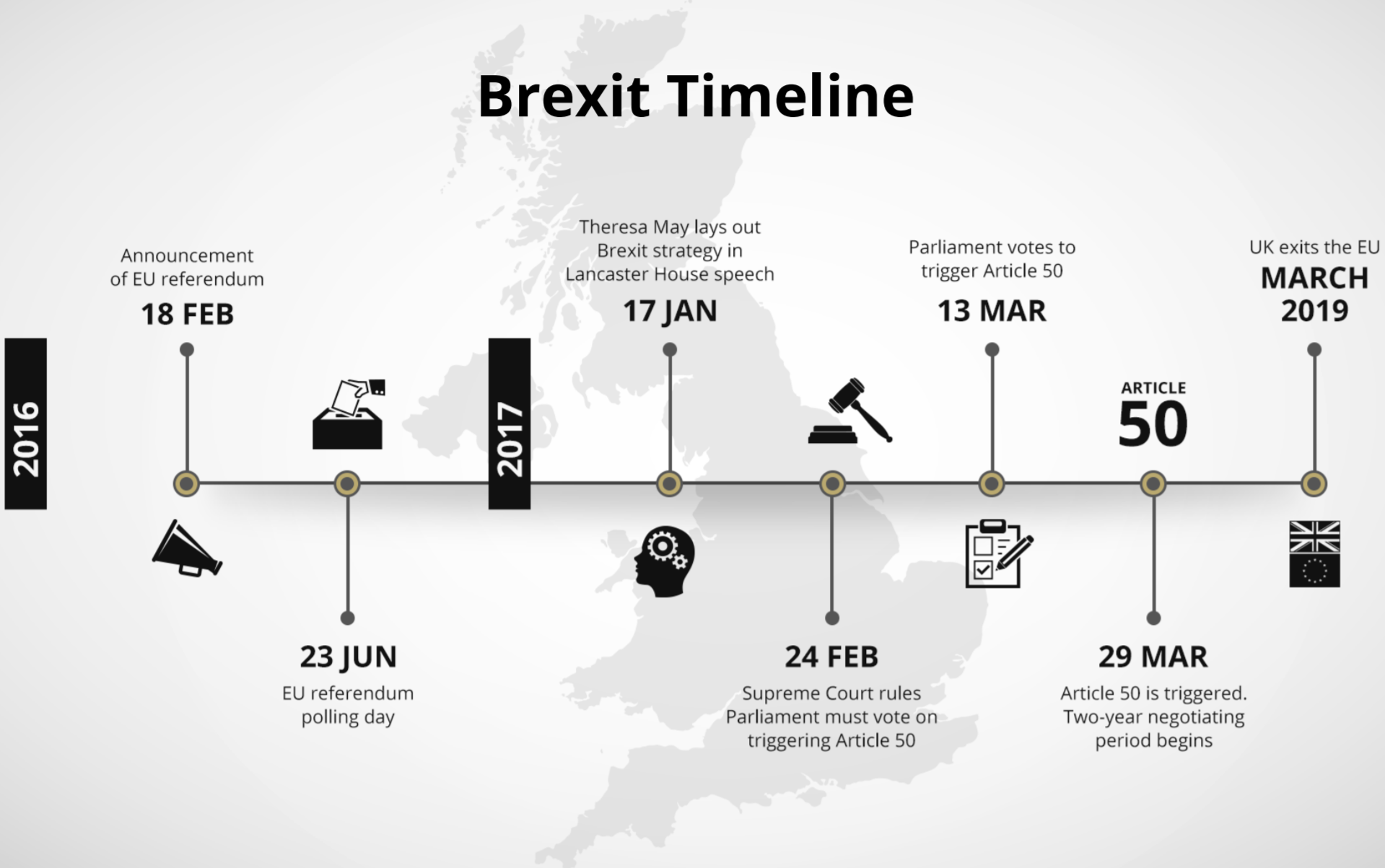

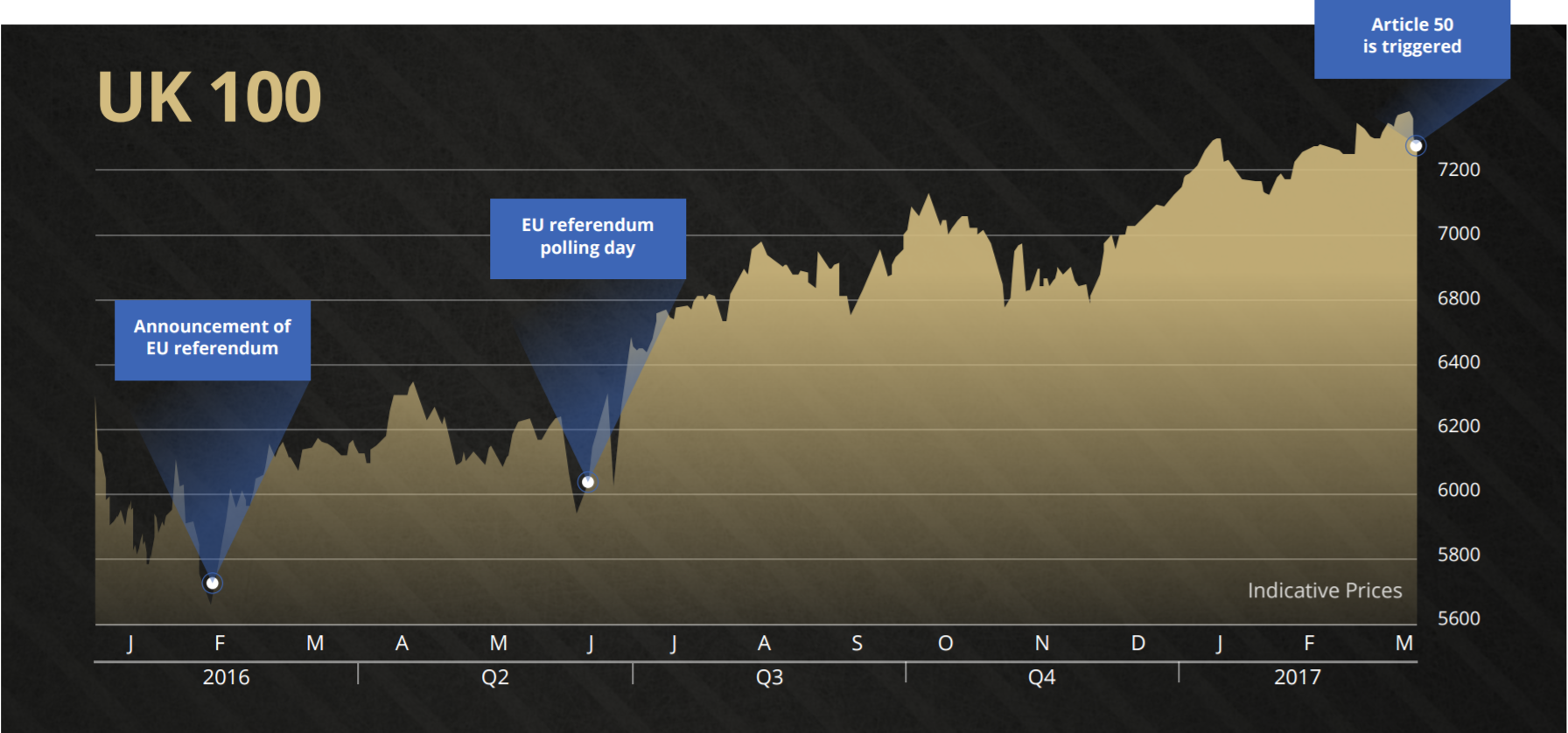

Britain’s vote to leave the European Union on June 23, 2016 (aka as Brexit) sparked an unprecedented wave of volatility in UK markets. The pound immediately plunged to its lowest in 30 years and has since suffered very large intra-day moves. The FTSE 100 cratered before turning course and enjoying one of its best ever rallies to achieve a series of record highs in early 2017.

All that before the process of exiting the EU had even started. So what can we expect from the markets as the Prime Minister triggers Article 50 – the formal mechanism for leaving the club?

In this paper we will look at some of the key ways in which exiting the EU will affect UK companies through the lens of the FTSE 100 index of leading shares, and sterling via the pound-dollar exchange rate.

Neil Wilson Senior Market Analyst at ETX Capital

Identifying Trading Opportunities

The Brexit vote itself produced unparalleled levels of volatility in some key markets, most notably sterling currency pairs and UK shares.

Here we look at two of the markets most exposed to the Brexit process:

Cable is the chief bellwether for market sentiment towards the UK and how the country is prospering. Since the June referendum the pound has slumped to 31-year lows despite the economy doing well. Growth has remained resilient and the price action has been determined more by the politics than the data. That’s made some of the usual assumptions about what drives GBPUSD somewhat redundant. Nevertheless, some key data like inflation remains central to our expectations of the pound’s direction.

GBP/USD

Cable is the chief bellwether for market sentiment towards the UK and how the country is prospering. Since the June referendum the pound has slumped to 31-year lows despite the economy doing well. Growth has remained resilient and the price action has been determined more by the politics than the data. That’s made some of the usual assumptions about what drives GBPUSD somewhat redundant. Nevertheless, some key data like inflation remains central to our expectations of the pound’s direction.

What’s driving the value of the Pound? Trade. Economy. Inflation and Interest Rates.

Trade

You can’t go very far talking about Brexit without the thorny issue of trade creeping in. At the heart of the exit process will be how Britain extricates itself from the single market and renegotiates trade terms with the EU. Tariffs would make British goods more expensive, therefore sterling has to weaken to balance this out. But there are also non-tariff barriers, such as customs checks, that could make the cost of doing business more. To remain competitive the pound has to be lower.

Examples of Tariffs on imports from outside the EU:

- Carrots – Importing from outside the EU is subject to a third country duty of 13.60% unless subject to other measures.

- Prosecco – Importing from outside the EU is subject to a third country duty of subject to tariff of $32 a hectolitre (32cents a litre)

The terms of Britain’s trade with the EU will also matter for trade with other nations. Britain says it wants to strike bilateral trade deals with non-EU countries but it cannot do that unless it leaves not only the single market but the looser customs union. Leaving the customs union without a new trade deal with the EU in place would see the UK default to WTO terms.

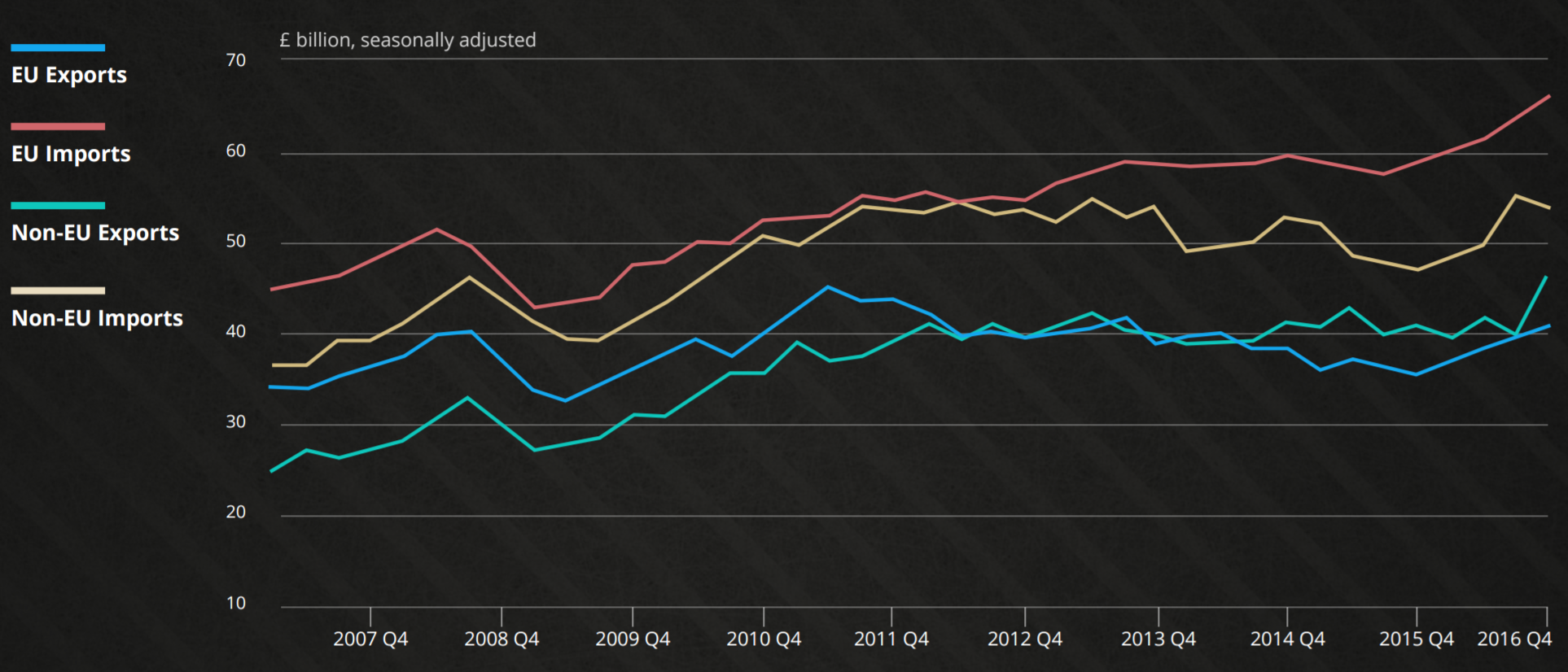

To see why the trade issue is so important to trading the pound, we have to come back to the basics of how the balance of trade is related to the exchange rate.

Exports quarterly contribution to growth by commodity

Currencies are affected by supply and demand and trade balances tell us how much demand there is for a particular currency. The more a country exports the greater the demand for its currency. This pushes up its value on the international markets as foreigners require more of the currency to purchase the goods and services it is exporting.

Of course when looking at exchange rates, we are in a sense looking into the future – what markets expect to happen. Therefore the fall in sterling can be seen as a simple recalibration of what constitutes the natural rate of exchange once Britain has left the EU – with the expectation that trading and transaction costs will be higher as British exporters become subject to new tariffs once outside the bloc.

Britain has been running a current account deficit for years and this has been financed by foreign capital – the ‘kindness of strangers’ that some describe. Markets expect Brexit to cause this flow to dry up, meaning the pound has to weaken to redress the imbalance. It is also a recalibration based on the attractiveness of the UK as an investment location. The pound has had to fall in order to make UK assets attractive. If Britain does have to go beyond Europe for investment then the pound might have further to fall. Leaving the single market will depress investment.

Financial Services

London has pulled in financial services activity and capital thanks to the economies of scale found in the City. But Brexit changes this.

Given that trade terms are likely to be worse than they are at present, Britain now faces the prospect of much higher transaction costs when doing business with the rest of Europe, which Paul Krugman notes “creates an incentive to move those services away from the smaller economy (Britain) and into the larger (Europe). Britain therefore needs a weaker currency to offset this adverse impact”. This is based on a simple economic model that states not all production (financial services in this case) will relocate to the large economy (the EU) as the small economy (UK ) is able make up for its lack of competitiveness by having a weaker currency.

The point is that the City is no longer located in the larger market, diminishing the flows of capital into the UK and therefore demand for sterling as businesses relocate to where it is cheaper to transact.

Property

The relationship of the UK property market and hot flows of capital to the sterling exchange rate is also important.

Since 2012 a property bubble in London drove an appreciation in sterling and a widening of the current account deficit. Double-digit rises in property prices pushed up the exchange rate and pound effectively became overvalued.

Brexit ended this trend and we have seen London prices cool markedly. Outflows from property funds surged in the wake of the referendum, forcing many to shutter to new withdrawals to prevent collapse.

Viewed through both of these examples, we can see that Britain was experiencing hot flows of cash into London (thanks to the City’s status) which drove up property prices and the value of sterling. Rising property values (seen as a safe haven for investors, again because of London’s pre-eminence as a global financial hub) fuelled further capital inflows in a version of the carry trade.

One of the most important considerations for valuing the pound is therefore the outcome for financial services from Brexit. Will the banks leave? Will London lose its status as Europe’s most important financial centre? The other – of course related – is the path of London property prices as a guide to sterling demand.

The Wider Economy

One of the most striking and surprising aspects of the UK economy after the referendum has been just how well it has stood up to the shock. Growth has remained solid and Britain was the fastest-growing G7 economy last year. A lot of this has been done to some remarkably resilient consumer spending.

Generally speaking, expectations of a decline in growth would drive currency weakness as, among other things, it suggests interest rates will remain low or need to be cut. The pricing of sterling post Brexit can also therefore be seen as markets expecting the wider UK economy to suffer. Forecasts vary and have been revised but the base case among most economists is for the UK economy to be smaller under Brexit than if Britain were to remain in the EU.

Only it hasn’t really started to decline, yet. A source of upside potential for sterling over the next 18-24 months will therefore be a resilient domestic economy that supports the case for rates to move higher.

UK GDP was estimated to have increased by 2.0% during 2016, slowing slightly from 2.2% in 2015 and from 3.1% in 2014.

Forecasts

The Bank of England has had to revise up its forecasts for 2017, upgrading its estimate to 2% for the year. Growth is expected to moderate in 2018 and 2019 still but the upward revision indicates that economists have got it wrong so far over the impact of Brexit on the economy.

That said, the real work starts now with the triggering of Article 50. The negotiations will tell us what sort of economy we will be left with and therefore the growth estimates could be revised significantly again.

At present, with sterling near its lowest in over 30 years, currency markets are still pricing in a fairly significant downward path for the UK economy. This could alter to the upside if growth remains strong and produce a slow and steady march higher for the pound. A cliff-edge departure from the EU with no trade agreements in place could result in a shock to the economy that sends sterling lower still.

Inflation and Rates

Lower for longer? The Bank of England slashed rates after the Brexit vote in a preemptive strike to calm the markets. While Carney’s critics say this was unnecessary, there is an argument that the post-Brexit resilience in the UK economy was boosted by the move. It’s all fairly moot now. The key is what the Bank expects of growth and inflation in the coming 18-24 months.

Growth, as discussed earlier, is holding up well. It could falter but a recession is no longer expected. The other driver for interest rates is inflation and that’s where there is a potential for the Bank of England to act.

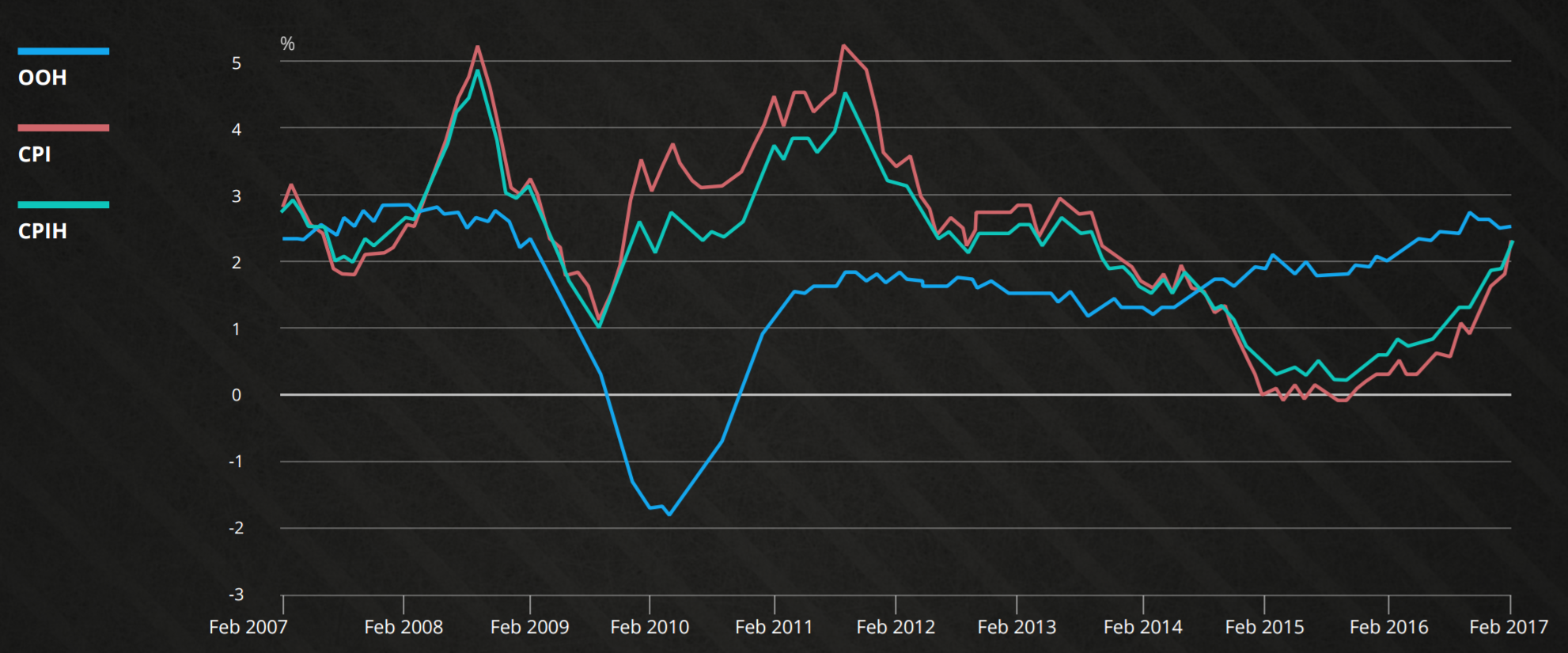

Inflation has accelerated post-referendum – in large part down to higher oil prices and the weak pound. It is less demand driven, although the strong consumer spending trend supports prices rising too.

The Bank could be minded to act if inflation overshoots. Governor Mark Carney has stressed that there are “limits to the extent an inflation overshoot can be tolerated”. At its March meeting the MPC delivered a somewhat hawkish surprise when one member, Kristin Forbes, voted to raise rates. It also suggested others were close to following suit: “Some members noted that it would take relatively little further upside news on the prospects for activity or inflation for them to consider that a more immediate reduction in policy support might be warranted.”

Shortly after inflation was revealed to have shot up to 2.3%, above the bank’s target. However, there are significant obstacles to hiking.

While growth is solid and inflation rising, we are not yet seeing the kind of upward pressure on wages that is needed to sustain gains in the underlying or core inflation rate. Aggregate demand is expected to slow and consumer spending is precarious. The MPC knows monetary policy is a fairly blunt tool and is not enough to combat the real adjustment required for new trading arrangements.

The bank noted that “attempting to offset fully the effect of weaker sterling on inflation would be achievable only at the cost of higher unemployment and, in all likelihood, even weaker income growth”. The point being that hiking rates to offset inflation carries a whole lot of other risks. This appears for now to be a sizeable hurdle to the Bank tightening, not least because the effect of a weaker pound on the annual gauges of inflation should start to fade by the end of 2017. Moreover, as inflation is less demand driven and the result of external factors (Currency, commodity prices), raising interest rates risks plunging the economy into a recession. However as we have seen the weather can change pretty rapidly.

CPIH, OOH and CPI 12-month inflation rate for the last 10 years

UK 100

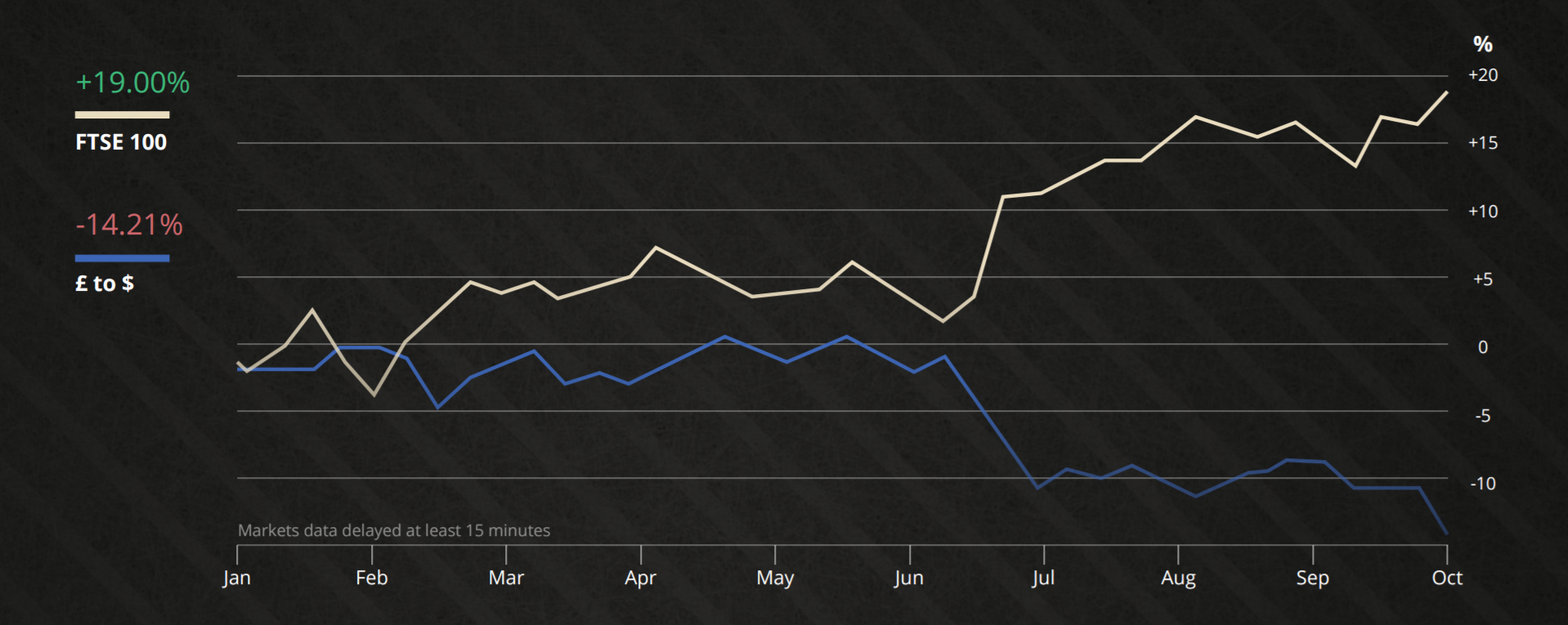

The trend is your friend? Certainly the trend since Brexit has been one of unalloyed buoyancy for the FTSE 100. To a large extent this has been down to sterling weakness because so many components are big dollar earners. But the correlation between sterling and the FTSE 100 is breaking down as the pound’s fall – now steadied – has become baked into equity valuations.

Increasingly as we head into 2017 the performance of individual shares and the index as a whole should be dictated by the details of Brexit. Which sectors will be hit, which companies are exposed? The devil will be in the detail. For anyone trading the FTSE’s rise off the back of pound weakness since June, the free ride is over.

Nevertheless, understanding the factors behind the FTSE’s rally tell us a lot about how to position trades through 2017 and beyond.

Naturally, there are many competing factors. Here we attempt to identify some of the most important. They touch on individual stocks (BP, Shell) which have an outsized effect on the index. We look at sectors and the prospects for earnings growth. We look at sterling and the crucial effect that the fall in the pound has had on the market. And we look at the political landscape and how that might directly affect companies on the FTSE 100.

MARKET WEIGHTING – the impact of some stocks is greater than others

You might be fairly familiar with index weights or you may never have heard of them. The point is to understand that in an index like the FTSE 100, the weighting plays a huge part. For instance, the FTSE is less likely to be affected by a big move in EasyJet shares than by a similar swing for the likes of HSBC or British American Tobacco.

Notable in the FTSE is the prevalence of dollar earners. As we have seen since the referendum, the fall in the value of the pound has corresponded closely with the rise for the FTSE 100 as the translation effect of converting dollar earnings into pounds for reporting is positive for balance sheets.

It’s not just the currency conversion effect that is driving shares higher. The weak pound makes UK shares cheaper for investors abroad. If you’re a pension fund manager in Frankfurt or a hedgie in New York, UK shares are cheaper than they were. In dollar terms, the FTSE 100 is still below pre-Brexit peaks.

Sterling

The leading FTSE 100 companies are dominated by dollar earners. In addition to the five listed earlier, the other big players are the likes of AstraZeneca, GlaxoSmithKline and Diageo as well as the large number of miners and commodity giants. Something like three-quarters to four-fifths of all FTSE 100 earnings are in dollars.

Long term traders may consider the trend of sterling when trading the UK 100. But for intra-day and other short-term traders, what is the correlation like?

Increasingly since the start of 2017 the correlation between the FTSE and the pound has become weaker – the long FTSE, short pound trade is harder to make as the pound has steadied. Now we have to consider how the details of the Brexit negotiations will affect individual companies and sectors.

Nevertheless, should there be another significant drop in the sterling exchange rate, we could expect to see a commensurate rise in the value of certain UK equities and the FTSE 100, led by its dollar earners. The complication arises from what might drive another drop in the pound. If trade terms turn out to be significantly worse we would expect the value of a wide range of stocks, including some of those dollar earners, to be affected.

Three of the most exposed sectors are retail, financial services and airlines. Brexit is just one factor affecting valuations, but potentially a vital one.

Retail

Short term, the two things most relevant for the sector are pound weakness and consumer spending. Neither have had much effect so far. Tesco fended off an attempt by Unilever to hike prices by 10% and currency hedging has insulated firms from some of the worst of the pound’s fall. Consumer spending has been resilient.

Looking ahead, however, the cost of goods purchased from abroad will rise as hedging contracts expire and retailers have to pay more. This will undoubtedly hit margins, particularly in the fiercely competitive supermarket sector where the big 4 (Tesco, Asda, Sainsbury’s and Morrisons) are loathe to raise prices as they battle discounters. Retailers will either have to take the hit or pass it on the customers. More than likely it will be a bit of both, which will have a dampening effect on margins and profit growth. Meanwhile, the rise in inflation, which has accelerated markedly in recent months, is likely to crimp consumer spending.

Longer term, considering the details of Britain’s exit negotiations, there are a number of important factors that will influence the performance of retailers over the next 2-3 years. For example, the dependency on a relatively high number of non-UK workers who may or may not be allowed to remain in the UK. Trade deals will also be important for sourcing goods at reasonable prices to sell to consumers.

Even if there is a trade deal of sorts, we can expect retailers to source more domestically. Morrisons published a report urging greater reliance on UK-sourced food. This would entail a higher average price.

Meanwhile, non-food retailers could enjoy a significant benefit from shoppers coming to Britain or shopping online to take advantage of the weak pound.

Financial Services

Maintaining ‘passporting’ rights for the thousands of City firms and large banks is seen as crucial for maintaining London’s position as the world’s pre-eminent financial hub. For large banks with a global footprint like HSBC or Standard Chartered, passporting rights are useful but not the end. They can simply move the operations they need to. Therefore the impact of Britain leaving either the single market or customs union may not be great on individual bank shares. Banks are pretty resilient in that sense.

Another outcome of the Brexit negotiations to consider is euro-denominated clearing, which is dominated by London. The European Central Bank would dearly love to freeze the City out.

But the most important thing for banks is the relationship between earnings and the economy – things like the UK housing market, consumer spending and so on. A pretty large number of shares on the FTSE are similarly exposed to the UK economy. If Brexit, either via the squeeze on living standards from the weak pound or a material drop in business activity, investment and earnings, (or both) leads to a fall in the UK economic outlook, we might just start to see the bullishness around UK bank shares fade.

Finally, the relationship between the UK economy and interest rates is of material importance for banks. Lower interest rates tend to reduce bank earnings. The longer the BoE keeps a lid on interest rates the tougher it will continue to be for banks to improve their earnings from interest.

Airlines

One thing is not in doubt – the impact of Brexit on the aviation industry is uncertain. Competing regulatory factors, the fall in sterling and the wider economic impact on demand for air travel make this a complex case. And it comes amid a turbulent time for the sector as low-cost carriers disrupt the market, oil prices rise again and strikes by staff in Europe dent profits for the big firms.

According to the International Air Transport Association (IATA), the effect of Brexit on the economy will see the UK air passenger market be 3-5% smaller by 2020. The weaker pound has an effect on demand, making outbound travel more expensive and inbound travel cheaper. For airlines it also affects things like average seat prices (eg Ryanair, which has large exposure to UK market but reports in euros), and fuel costs, as oil is priced in dollars.

In terms of the details of the exit talks it is the regulatory environment that is most affected. And perhaps the most important aspect of this is whether the UK will remain in the Single Aviation Market or, by extension, part of the EU-US Open Skies agreement.

The IATA noted: “Depending on the terms of exit, these agreements would potentially cease to apply to the UK, possibly requiring the UK to negotiate a whole raft of separate bilateral agreements. In theory, this could be a positive in some cases, giving the UK greater flexibility to negotiate agreements suited to the best interests of UK consumers. However, as a single country the UK would lack the bargaining power of a 500-million population trading bloc such as the EU.”

In other words, UK-based carriers may be forced to take costly measures to remain part of these agreements. Meanwhile the cost of flying in and out of the UK from the EU and US could rise, should there be no corresponding deal for airlines. More costly air travel could further dent outbound travel demand and hurt margins. Therefore we could see, should the terms of exit be worse than they currently, a material decline in revenues and profits for airlines. The likely impact of any new trade deals with nations outside the EU is hard to quantify but is unlikely to produce a noticeable uplift in travel within the next two years given that no such agreements are possible while the UK is still a member of the EU

{kind=link}